What Is Skewness And Kurtosis In Finance. If these assets are temporally aggregated both will disappear due to the law of large numbers. Sep 28 2020 Summary.

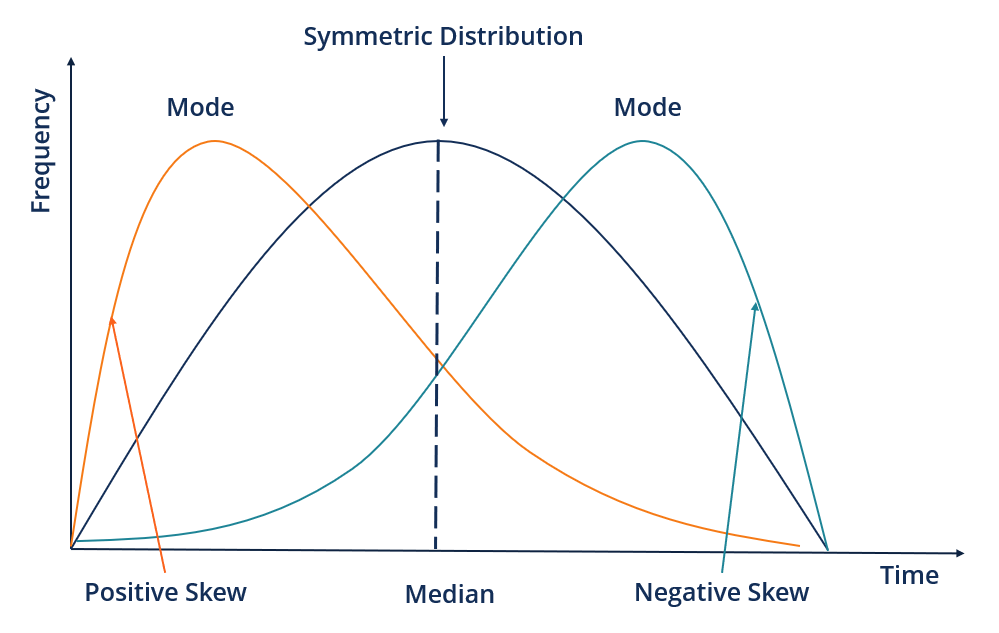

Of the tails of a distribution. While skewness is a measure of asymmetry kurtosis is a measure of the peakedness of the distribution. Sep 28 2020 Summary.

DEFINITION of Kurtosis Like skewness kurtosis is a statistical measure that is used to describe distribution.

Both skewness and kurtosis are measured relative to a normal distribution. If the coefficient of kurtosis is larger than 3 then it means that the return distribution is inconsistent with the assumption of normality in other words large magnitude returns occur more frequently than a normal distribution. HttpwwwstatberkeleyedustatlabsdatababiesdataHere I show you how to understand numbers for skewness and kurtosis with some examp. Under Assumption 13 KEN 77 provide the distribution of the sample estimators ŝ and k.